IBRSiQ March 2026

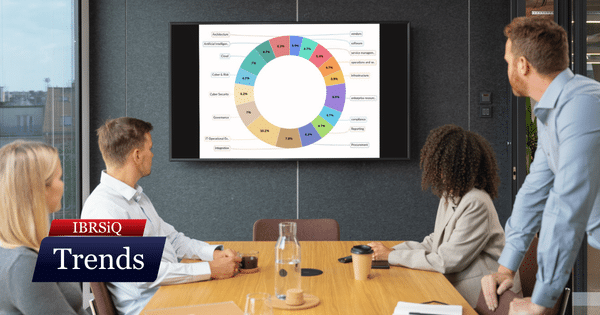

In March, clients are prioritising AI-driven operational efficiency, cyber maturity, and ERP optimisation while ensuring ICT investments deliver measurable, strategic business value.

In March, clients are prioritising AI-driven operational efficiency, cyber maturity, and ERP optimisation while ensuring ICT investments deliver measurable, strategic business value.

Australia’s AI Plan prioritises sovereign capability and green data centres, yet lacks funding and mandatory regulation to ensure public trust.

February focuses on pivoting from adoption to pragmatics, prioritising operational excellence, rigorous AI governance, and cost-optimised infrastructure to secure tangible value.